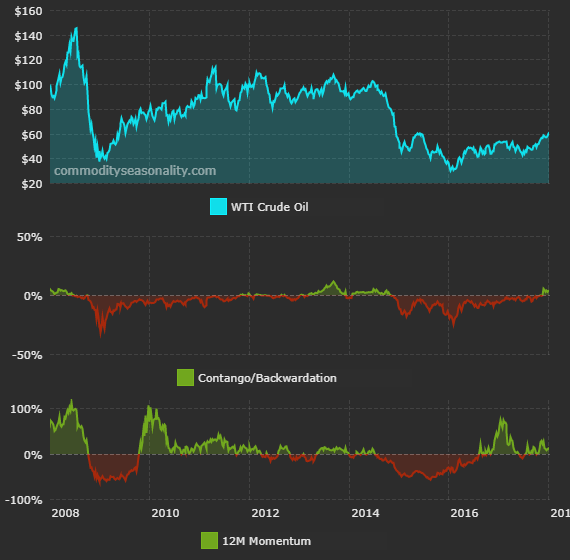

In the world of commodities trading, the concept of backwardation is a key indicator of market trends and investor sentiment. In recent times, the West Texas Intermediate (WTI) oil market has been experiencing a state of backwardation, sparking discussions and debates among industry experts. The question on everyone’s mind is whether this backwardation in WTI is temporary or indicative of a larger trend shift.

Understanding the dynamics of backwardation is essential in grasping the current state of the WTI market. Let’s delve deeper into this phenomenon to gain insights into what the future may hold for WTI prices.

The Basics of Backwardation

First and foremost, it is crucial to have a clear understanding of what backwardation entails in the context of commodities trading. Backwardation occurs when the spot price of a commodity is higher than the futures price. This situation suggests that the market anticipates a decrease in the price of the commodity over time.

Historically, backwardation has been associated with supply shortages, geopolitical uncertainties, or abrupt shifts in market conditions. It reflects a sense of urgency in acquiring the commodity in the present moment rather than waiting for future deliveries.

WTI Backwardation: A Temporary Phenomenon?

The recent backwardation observed in the WTI market has raised concerns among traders and investors. Some believe that this phenomenon is merely a temporary imbalance caused by short-term factors such as weather disruptions, production cuts, or geopolitical tensions.

However, others argue that the sustained backwardation in WTI prices could signal a more profound shift in market dynamics. Structural changes in the oil industry, evolving demand patterns, or regulatory developments may be contributing to the prolonged backwardation in WTI.

Implications for Investors and Traders

For investors and traders in the WTI market, the question of whether the current backwardation is temporary or a long-term trend shift is of utmost importance. The decision to buy, sell, or hold WTI contracts relies heavily on accurately predicting the future direction of prices.

If the backwardation in WTI is indeed temporary, investors may choose to capitalize on short-term price discrepancies and generate profits from market arbitrage. On the other hand, if the backwardation signals a broader trend shift, strategic portfolio adjustments and risk management strategies may be warranted.

The Role of Market Fundamentals

Examining the underlying market fundamentals is essential in deciphering the root causes of WTI backwardation. Factors such as production levels, inventories, demand projections, and geopolitical risks all play a significant role in shaping the trajectory of WTI prices.

Supply Dynamics

The supply-side dynamics of the oil market have a direct impact on WTI pricing. Production levels, OPEC+ agreements, shale oil output, and global macroeconomic conditions all influence the supply-demand equilibrium. Any disruptions in supply chains or unexpected production fluctuations can trigger fluctuations in WTI prices.

Demand Trends

Understanding demand trends is equally critical in assessing the sustainability of WTI backwardation. Economic growth prospects, energy policies, technological advancements, and consumer behavior patterns all shape the demand for crude oil. Shifts in demand dynamics can exert significant pressure on WTI prices.

Geopolitical Risks

Geopolitical factors have always been a wildcard in the oil market, impacting prices and market sentiment. Events such as political unrest, trade disputes, sanctions, or conflicts in oil-producing regions can lead to supply disruptions and volatility in WTI prices. Investors must monitor geopolitical developments closely to gauge their impact on the WTI market.

The Future of WTI Backwardation

As the debate over the nature of WTI backwardation continues, the future remains uncertain. While short-term factors may be driving the current state of backwardation, long-term trends could reshape the dynamics of the WTI market in the coming years.

Investors, traders, and industry observers need to stay vigilant, analyze market data, and assess risk factors to navigate the complexities of the WTI market successfully. Whether the backwardation in WTI is a temporary anomaly or a harbinger of significant market shifts, one thing is certain – adaptability and foresight are vital in thriving in the ever-evolving world of commodities trading.