In the realm of financial economics, one concept that continues to intrigue and puzzle scholars is the credit multiplier. Often misunderstood and overlooked, the credit multiplier plays a crucial role in the functioning of modern banking systems. In this comprehensive analysis, we delve deep into the intricacies of the credit multiplier, its significance, and its implications on the broader economy.

The Genesis of the Credit Multiplier

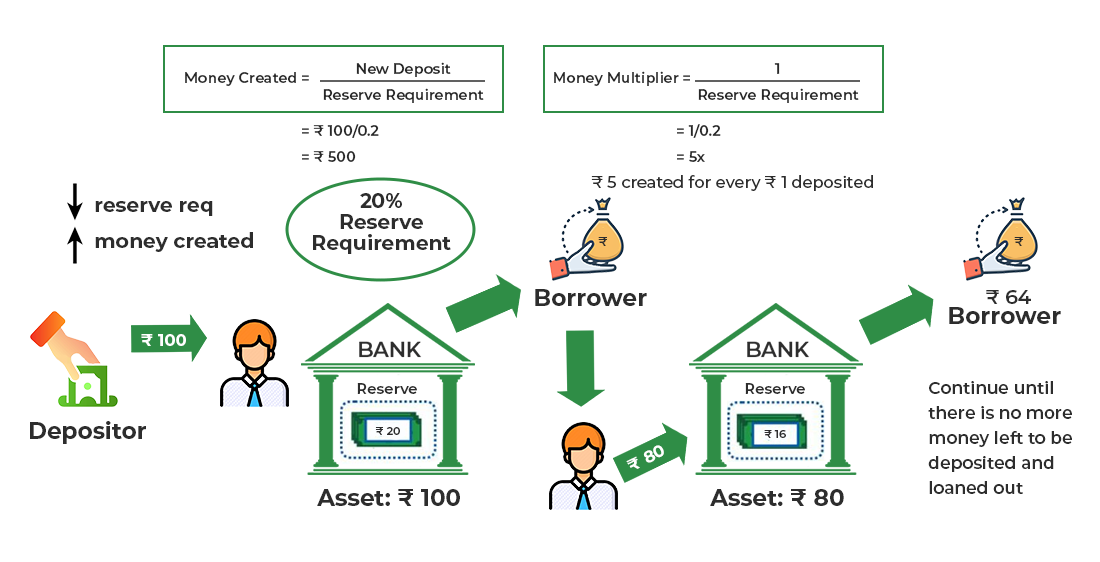

At the heart of the credit multiplier lies the concept of fractional reserve banking. In a fractional reserve system, banks are only required to hold a fraction of their deposits in reserve, allowing them to lend out the remaining amount. This practice creates a multiplier effect on the initial deposit, leading to an expansion of the money supply. The credit multiplier is essentially the ratio of the increase in money supply to the initial deposit. Understanding the mechanics of the credit multiplier is essential to grasping its impact on the economy.

The Mechanism in Action

When an individual deposits money into a bank, the bank is able to lend out a portion of that deposit while keeping the rest as reserves. This process sets off a chain reaction, as the borrower may then deposit the loan amount into another bank, which in turn lends out a portion of that deposit. This cycle continues, with each iteration leading to an increase in the money supply. The credit multiplier is a powerful force that has the potential to significantly amplify the impact of initial deposits on the economy.

The Role of Commercial Banks

Commercial banks play a central role in the credit multiplier process. By accepting deposits and extending loans, banks facilitate the flow of funds within the economy. Through the creation of credit, banks are able to spur investment, consumption, and overall economic activity. However, the credit multiplier is not without its risks. Excessive lending by banks can lead to over-leveraging and financial instability, as seen in past banking crises.

The Impact on Monetary Policy

Monetary policymakers closely monitor the credit multiplier when formulating policy decisions. By adjusting interest rates and reserve requirements, central banks can influence the money supply and, by extension, the credit multiplier. Understanding the dynamics of the credit multiplier allows policymakers to fine-tune their policy tools to achieve specific economic objectives, such as controlling inflation or stimulating growth.

The Global Perspective

While the concept of the credit multiplier is universal, its implementation and implications can vary across different countries and regions. Developing economies may face unique challenges related to capital flows, exchange rates, and financial stability. The credit multiplier can have far-reaching effects on the global economy, influencing trade, investment, and overall economic growth.

The Evolving Landscape

With the advent of digital payments and fintech innovations, the traditional banking system is undergoing rapid transformation. New technologies such as blockchain and cryptocurrencies are reshaping the way financial transactions are conducted. The credit multiplier may take on new forms in the digital age, posing both opportunities and challenges for policymakers and economists.

The Road Ahead

As we navigate the complexities of the credit multiplier, one thing remains clear: its impact on the economy cannot be underestimated. By studying its mechanisms, implications, and evolution, we gain valuable insights into the intricate workings of the financial system. The credit multiplier stands as a testament to the interconnectedness of financial markets and the enduring quest for economic stability and prosperity.