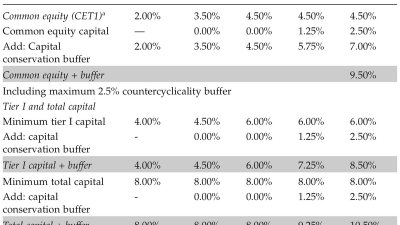

As a Music Journalist with a conservative tone of voice and a journalistic writing style, it is crucial to delve into the topic of capital allocation within the realm of finance. Efficient capital allocation plays a vital role in the success of an individual or organization’s financial portfolio. In this in-depth analysis, we will explore the importance of efficient capital allocation and its implications on overall financial performance.

The Fundamentals of Capital Allocation

Efficient capital allocation involves the strategic distribution of resources to optimize returns and minimize risks. It is a fundamental concept in finance that underpins the decision-making process for investors, businesses, and financial institutions.

The Impact of Efficient Capital Allocation

Effective capital allocation is essential for maximizing shareholder value and ensuring the long-term viability of an organization. By allocating capital efficiently, companies can invest in projects with the highest potential returns, thereby increasing profitability and driving sustainable growth.

Strategies for Efficient Capital Allocation

There are various strategies that can be employed to enhance capital allocation efficiency, including diversification, risk management, and performance monitoring. By implementing these strategies, individuals and organizations can make informed decisions about where to allocate their capital for optimal results.

The Role of Asset Allocation

Asset allocation plays a critical role in efficient capital allocation by determining the optimal mix of assets within a portfolio. By diversifying investments across different asset classes, investors can reduce risk and enhance returns. Asset allocation is a strategic approach that aims to balance risk and reward based on individual investment goals and risk tolerance.

Challenges in Capital Allocation

Despite the benefits of efficient capital allocation, there are challenges that can hinder its effectiveness. These challenges may include market volatility, regulatory constraints, and limited access to information. Overcoming these obstacles requires a proactive approach to risk management and a focus on long-term financial goals.

The Importance of Risk Management

Risk management is a key component of efficient capital allocation, as it helps investors and organizations mitigate potential losses and protect their assets. By assessing and managing risk effectively, individuals and businesses can make informed decisions about where to allocate their capital to achieve their financial objectives.

Measuring Performance and Rebalancing

Monitoring performance is essential for evaluating the effectiveness of capital allocation strategies and making adjustments as needed. By periodically reviewing portfolio performance and rebalancing assets, investors can ensure that their capital is allocated in line with their investment objectives and risk tolerance.

Conclusion

In conclusion, efficient capital allocation is a fundamental principle in finance that drives financial success and sustains long-term growth. By strategically allocating resources, managing risk, and monitoring performance, individuals and organizations can optimize their financial portfolios and achieve their investment goals. It is imperative for investors to understand the importance of efficient capital allocation and implement sound strategies to maximize returns and minimize risks in today’s dynamic financial landscape.